Performance

The resilience of the U.S. economy helped to forestall a recession in the first quarter of 2023, bucking conventional wisdom and leading to positive stock and bond performance. The most out of favor stocks from last year – large cap tech – experienced the biggest resurgence in early 2023. Assets performed well across the board, with the exception of commodities, which tumbled over the first quarter. The banking sector difficulty in March has tempered expectations for the second half of the year, because the likely reduced availability of credit as a result could prove to be a headwind for economic growth over the next 6-12 months. Inflation continued to ease a bit, providing some respite for bonds, even as the Federal Reserve continues their path of interest rate hikes. Alternative assets fell in the first quarter, as small positive performance in real estate and natural resource stocks could not overcome the drag from commodities.

Stocks

Although both international stocks (MSCI All Country World Index ex-U.S.) and U.S. stocks (Russell 3000) advanced this quarter, U.S. companies eked out a slight performance advantage. Stronger-than-expected U.S. GDP growth in the first quarter helped bolster performance at home, while a less severe winter in Europe helped prevent fears of an energy crisis that could have cascaded through international economies from materializing. Large-sized (S&P 500) U.S. companies resumed their leadership position, outperforming small-sized (S&P SmallCap 600) and mid-sized (S&P MidCap 400) ones. Overseas, developed markets (MSCI EAFE) stocks rode better than expected European performance to outperform their emerging markets (MSCI EM) counterparts this quarter.

Bonds

Although the Federal Reserve continued to raise short-term interest rates this quarter, the slower pace of those increases and a decline in the inflation rate helped bonds (Bloomberg US Aggregate Bond Index) return positively. After a rough 2022, bonds have recovered some lost ground as a result of both higher income payments and from increased demand as a ballast against stock volatility.

Alternatives

Alternative assets were down 1.4% for the quarter. Natural resources stocks (S&P Global Natural Resources) and global real estate (FTSE EPRA/NAREIT Developed) eked out positive returns, but the larger negative performance from commodities (Bloomberg Commodity) pushed the asset class into negative territory.

Perspective

“Bank confidence is a fragile reed, and a troubled bank is damaged by any rumors, true or not.”

– Irvine Sprague, former FDIC Chairman

The very nature of our fractional reserve banking system leaves open the possibility of bank complications if depositors’ belief is shaken in the stability of an individual bank or the system as a whole. The recent downfalls of Silicon Valley Bank (SVB) and Signature Bank demonstrated that a crisis of confidence can happen in any institution. What appeared to be rock-solid investments in U.S. Treasuries ultimately led to the fall of SVB when interest rates shot up too high – and then depositors wanted their money back, quickly. The diminished value of those longer-maturity Treasury securities compared to their original amounts made it impossible for SVB to provide depositors their money back.

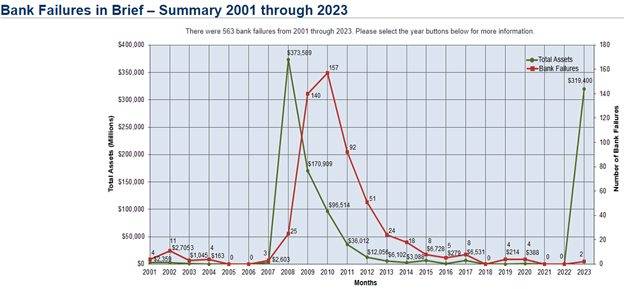

As concerning as the recent spate of problems in the banking industry are – from institutional collapses, to Federal Reserve and Treasury “rescue” plans, to larger institutions attempting to shore up confidence in struggling regional banks via capital infusions – this is not as uncommon an occurrence as one might think. There have been 563 bank failures since 2001. While most were clustered around the large-scale recession of 2008, there have typically been a handful of failures per year – albeit with relatively low asset volumes.

What made the SVB failure stand out was the relatively high level of assets controlled by the bank, the concentration of early stage high-tech companies within their depositor base, and the relatively new phenomenon of depositors being able to transact on their deposits electronically. The Federal Reserve and the U.S. Treasury Department have both attempted to shore up confidence in the sector as a whole, through the use of various stabilization funding tools. It appears that the banking system as a whole is clear of imminent complete disaster; however, there is always the possibility that other institutions could face trouble as the Fed continues its rising interest rate regime.

A positive surprise over the first quarter was the sizable gains enjoyed by stocks and bonds, as they recovered some from their drop of 2022. Economies in the United States and throughout the world proved more resilient than expected at the beginning of the year. U.S. GDP growth rebounded in the first quarter, inflation continued to tick downwards, and the labor market remained particularly strong. The European winter was relatively mild – short-circuiting the potential for a severe recession that could have been caused by skyrocketing energy costs.

But is the positive first quarter (welcome as it may be) just delaying the inevitable recession until later in 2023 or early 2024? I’d peg the chances at a solid maybe. There’s a good reason the old adage is “don’t fight the Fed.” As long as the Federal Reserve continues to raise interest rates to dampen economic demand to reduce inflation, the headwinds will be in place that have typically led to recessions in the past. Warning signs are present: an inverted yield curve (where short-term rates are higher than long- term rates), lower corporate earnings, and the steady decline in the level of Leading Economic Indicators (LEI).

While it is not a foregone conclusion that we will enter into recession over the next 12 months, the above signals have combined with the Fed’s own projections to paint a pessimistic outlook. At their March meeting, the Fed published expectations for the unemployment rate to increase by a full percentage point over the remainder of 2023 and for GDP growth to end at 0.4% for the entirety of 2023, which would require a contraction over the final three quarters. This sounds like the Fed’s base case is for recession before the end of the year. If the banking sector stress results in tighter lending requirements and a subsequent crunch in the availability of credit for businesses and consumers, this would only increase the likelihood of economic challenges.

Positioning

For all of these reasons, we are still maintaining a cautious approach to our asset allocation, with a slight underweight to both stocks and bonds relative to our benchmark weighting. We’ve been carrying the difference in money market funds for the past few months, content to earn a reasonable return as we analyzed the path forward for the economy and asset prices. Although our positioning has detracted from performance thus far in 2023 as stocks have marched higher, we still feel that it is prudent to guard against an economic downward turn later this year, and that our more cautious approach to stock exposure will end up being additive. Within our current stock holdings, we continue to emphasize our key tenet of diversification across a broad swath of sectors and geographies, while maintaining an emphasis on companies undervalued by the market and those with higher probability of predictable cash flows.

We have used the first quarter as an opportunity to enhance our bond offerings to provide additional solutions for client. We have partnered with Goldman Sachs, a leader in fixed income investing, to offer a separately managed account (SMA) to provide tax-efficient, individual ownership of bonds while providing a more predictable outcome due to its hold-until-maturity focus. For clients with predictable income needs, we offer bond ladders to match availability of cash to a schedule. We also continue to offer a solution comprised of funds for those clients who prefer to use that approach instead of individual securities. Please contact your advisory team to investigate which approach may be best for your circumstances.

As the Federal Reserve gets closer to the end of their short-term rate hike cycle, we are actively searching for the proper time to bring bond allocations to neutral positioning from underweight. Bonds have become more attractive due to the higher income component of total return; the capital appreciation component could enhance total return when the Fed stops hiking (or even cuts) rates. Money market yields would become less appealing in that instance – likely making a shift back into bonds additive.

We know that investing can sometimes feel like a roller-coaster ride, especially when unexpected shocks (such as bank failures) arise. However, relying on a sound financial plan developed with your specific goals in mind can help provide reassurance in tumultuous times. Helping to build your plan and marrying it with an individualized investment portfolio – while maintaining a dedication to diversification and cost sensitivity – is the hallmark of our company. We value the trust you’ve placed in us to assist you in your financial journey.

Please contact us with questions, or just to chat!