Performance

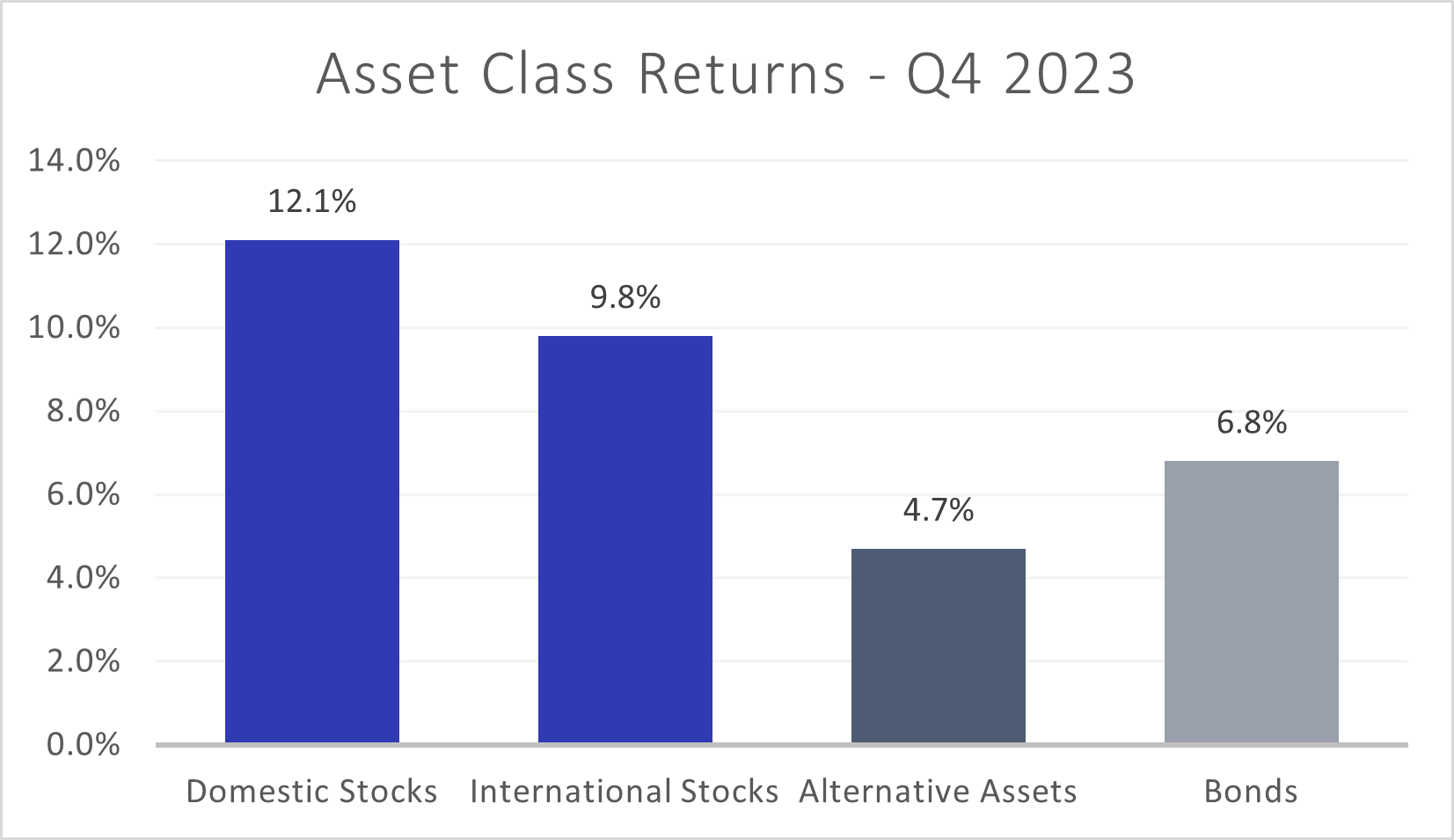

In a sharp reversal from the third quarter, a large majority of asset and sub-asset classes experienced gains in the final three months of 2023. Stocks rallied higher, based on hopes that the elusive “soft landing”– raising rates to quell inflation while simultaneously staving off a recession – can be achieved by the Federal Reserve. While it is too soon to declare victory in that effort, expectations for short-term interest rate cuts by the Fed beginning in early 2024 helped propel stock prices toward record highs in December. Bonds also flourished in the fourth quarter, as longer-term interest rates declined sharply in November (bond prices and interest rates typically move in opposite directions). Alternative assets scratched out a positive return for the quarter, even as commodities lost ground.

Stocks

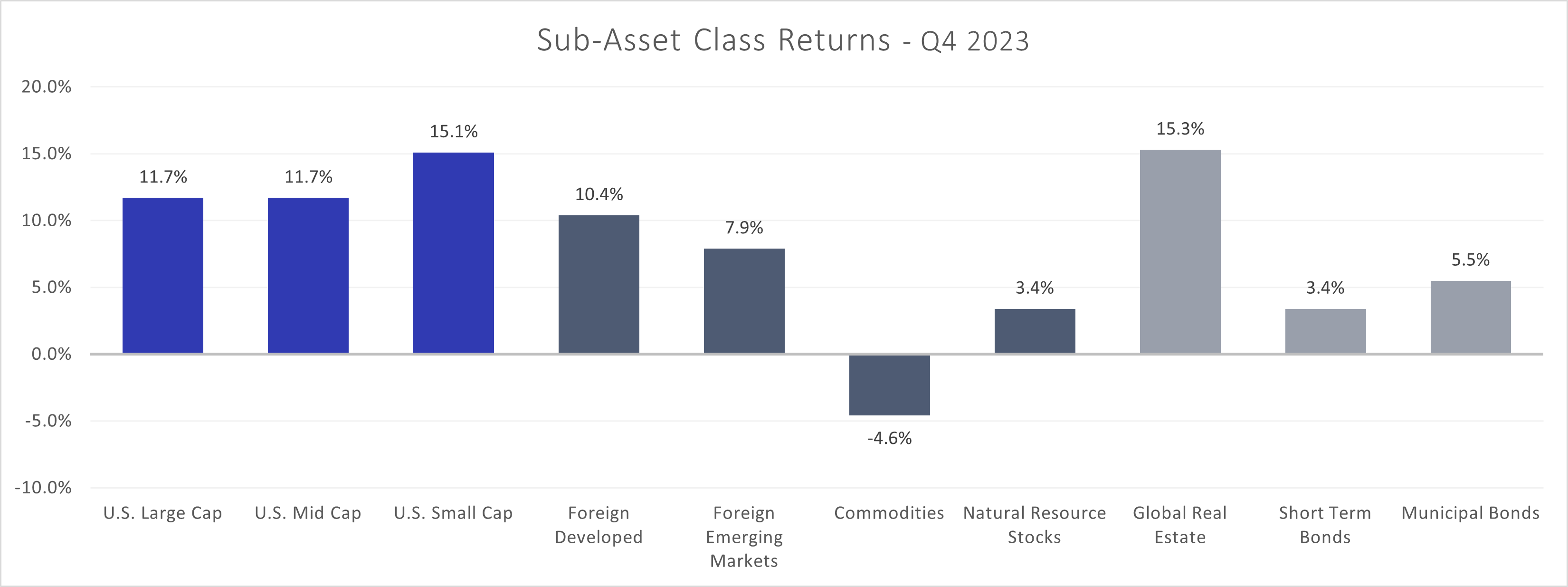

While worldwide returns were strong across every region, U.S. stocks (Russell 3000) again outpaced the performance of international stocks (MSCI All Country World Index ex-U.S.). Full year returns also favored U.S. companies, as the “Magnificent Seven” tech stocks drove the domestic market to heights that international companies could not match. Small-sized (S&P SmallCap 600) U.S. company stocks outperformed their large-sized (S&P 500) and mid-sized (S&P MidCap 400) counterparts over the quarter. Developed markets (MSCI EAFE) stocks grew faster in the fourth quarter than emerging markets (MSCI EM) companies; the continued economic struggles of China weighed down the overall emerging markets results on a relative basis.

Bonds

Bonds (Bloomberg US Aggregate Bond Index) posted their best monthly return in nearly 40 years in November, helping the broad index to flip the script and turn a sluggish 2023 into a healthy positive calendar year gain. As inflation declined and GDP growth expectations moderated, long-term bond yields declined, helping to fuel the gains. Indications from the Fed that rate cuts are possible in 2024 added to the positive feelings surrounding bonds. The combination of higher interest payments than in previous years and the potential for capital appreciation if and when the Fed cuts short-term rates this year make bonds an attractive alternative to cash.

Alternatives

Alternative assets rose in the fourth quarter, even though commodities (Bloomberg Commodity) posted a negative contribution as oil prices fluctuated. Global real estate (FTSE EPRA/NAREIT Developed) rose substantively from the third quarter, while natural resources stocks (S&P Global Natural Resources) gained to a lesser degree.

“Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.” – Paul Samuelson

Renowned U.S. economist Paul Samuelson was the first American to win the Nobel Prize in Economic Sciences. Having served under multiple Presidents and as a faculty member at some of the most prestigious higher education institutions, his career was quite distinguished. His quote about “excitement” in the market is relevant today; occasionally, clients will comment to us on the stereotype that investing is analogous to gambling.

While some types of investments can feel as risky as the roulette table, a solid investment strategy will employ key elements that help minimize the mystery and intrigue of extreme fluctuations, investment jargon, and blaring news headlines. This is especially true as we enter the new year, and questions abound related to the impact of political strife and major military conflicts as well as the future direction of monetary policy and inflation … the list goes on and on. It will be as important as ever to hold fast to the disciplines (as outlined in the Positioning section below) that promote long-term success amid chaos. Against that background, here are some things we will be scrutinizing particularly closely in 2024.

Inflation and monetary policy

The steep rise in stock prices at the end of 2023 indicates the market is increasingly trusting that the Fed has engineered a “soft landing” via monetary policy. It’s premature to declare victory. The final downward leg towards the Fed’s goal of 2% inflation must still be maneuvered, and the cumulative effect of more than 5% of short-term interest rate hikes over the past two years on consumer demand has not yet fully been felt. While there is still a chance that we won’t see a recession in 2024, history makes a good case that the substantial increase in rates since March 2022 will eventually force unemployment higher and choke off growth – inducing a recession in the process.

Global growth

Speaking of economic growth, U.S. GDP is projected to slow from the highs of third quarter 2023 based on the lagged effects of monetary policy, exhaustion of excess COVID-era savings, and businesses cutting back on production. Globally, the International Monetary Fund (IMF) has forecasted a slight decline in worldwide GDP growth from 3.0% to 2.9% in 2024. With the geopolitical situation appearing daunting in 2024 (see below), these projections could be upended in very short order if ongoing conflicts further intensify, or new disputes arise and derail the global economy.

Geopolitics

The Ukraine war, ongoing military conflict in the Middle East, U.S. confrontations with China and Iran – there is no shortage of political wild cards currently on investors’ dockets. Additionally, there is the matter of a near-certain contentious U.S. Presidential election this year. While there is always something going on in the world that affects markets, this year could be more intriguing than usual. To make sense of the current situation, please join us for our Outlook event on January 25 at 11 a.m. EST with guest speakers Matt Gertken and Mo Wright. Sign up here.

Outlook for stocks and bonds

Of course, we cannot know precisely how major global events will affect asset prices this year, but the below chart shows that historically, early in the primary season of election years has been more volatile for stocks before trending in a positive direction in the second half.

The range of opinions regarding stock returns in 2024 is wide and varied. A bullish case can be made as easily as a bearish one. Slowing inflation, a still-strong labor market, vast money market reserves ready for deployment to other asset classes, and a signaled Fed easing of rates in 2024 boosted stock prices in the fourth quarter of 2023 and could continue to lead prices higher. On the other hand, the decline in manufacturing output, record high credit card balances, inflation still not at the Fed target, and projected lower GDP growth are all potential red flags.

Bonds seemingly have a clearer path to positive returns in 2024. The combination of higher interest payments, the potential for capital appreciation if rates decline, and a potential increase in demand for bonds if stocks suffer declines all point to a positive 2024 for bonds in most economic environments.

Positioning

Our key tenets of investing – practicing asset allocation, diversifying globally, maintaining a sensitivity to cost, and marrying client investment strategy with their financial plan – may not sound “exciting.” But they are the tried-and-true principles we utilize to help clients meet their financial goals, and are especially vital when facing an outlook as opaque as we all are in 2024.

Rather than employ a strategy that seeks to maximize returns regardless of risk, we have long focused on risk mitigation. The hallmark of our investment philosophy is utilizing various asset classes and focusing on multiple regions as our core portfolio construction strategy, while giving ourselves the flexibility to tilt in and out of asset class and sub-asset class categories. While this approach can sometimes lead to underperformance in narrowly concentrated market conditions, over the long run we feel that it is the best way to mitigate the risk of extensive downside losses.

When deciding on how to fine-tune client portfolios (stocks vs. bonds, growth vs. value, U.S. vs. International, etc.), we seek to make decisions while considering a 12-to-18-month time horizon. This helps guard against chasing the latest “hot” strategy or simply choosing the best recently performing asset. Rather, we look to tweak portfolios where longer-run effects appear to be in play. Such recent adjustments include: swapping out our emerging markets index fund for one that excludes Chinese stocks due to systemic issues, boosting our domestic stock exposure on the relative strength of the U.S. economy compared to other nations during this period of market instability, and reconstructing our bond funds to afford greater flexibility in dealing with a rapidly changing interest rate environment – all of which were additive in 2023. While our core exposures provide the overwhelming source of returns, it is this subset of choices that affords us the potential for above-benchmark returns.

Of course, there is always the chance that our interpretations detract from performance. We were underweight stocks relative to benchmark for most of 2023. Although our absolute performance was still quite strong this year, as stocks ripped higher on exceptional performance from large cap tech stocks, we lagged relative to benchmark. But we’d prefer to give up a bit of upside potential in a roaring market to help guard against large losses in a downturn. That’s why as we enter 2024 we are still cautious about the economy and near-term path for stock returns. For now, we remain slightly underweight in stocks and will look to redeploy the funds we hold in still strong money markets when a better opportunity presents itself.

In the meantime, we suggest you take stock of whatever cash needs you have for the upcoming year, ensure that you have enough to cover those needs (trimming some fourth-quarter gains, if necessary), and let us help you examine your financial situation. We can help determine if anything has changed that would warrant amending your plan. This is a perfect time to make any necessary adjustments.

Please contact us with questions, or just to chat!