Performance

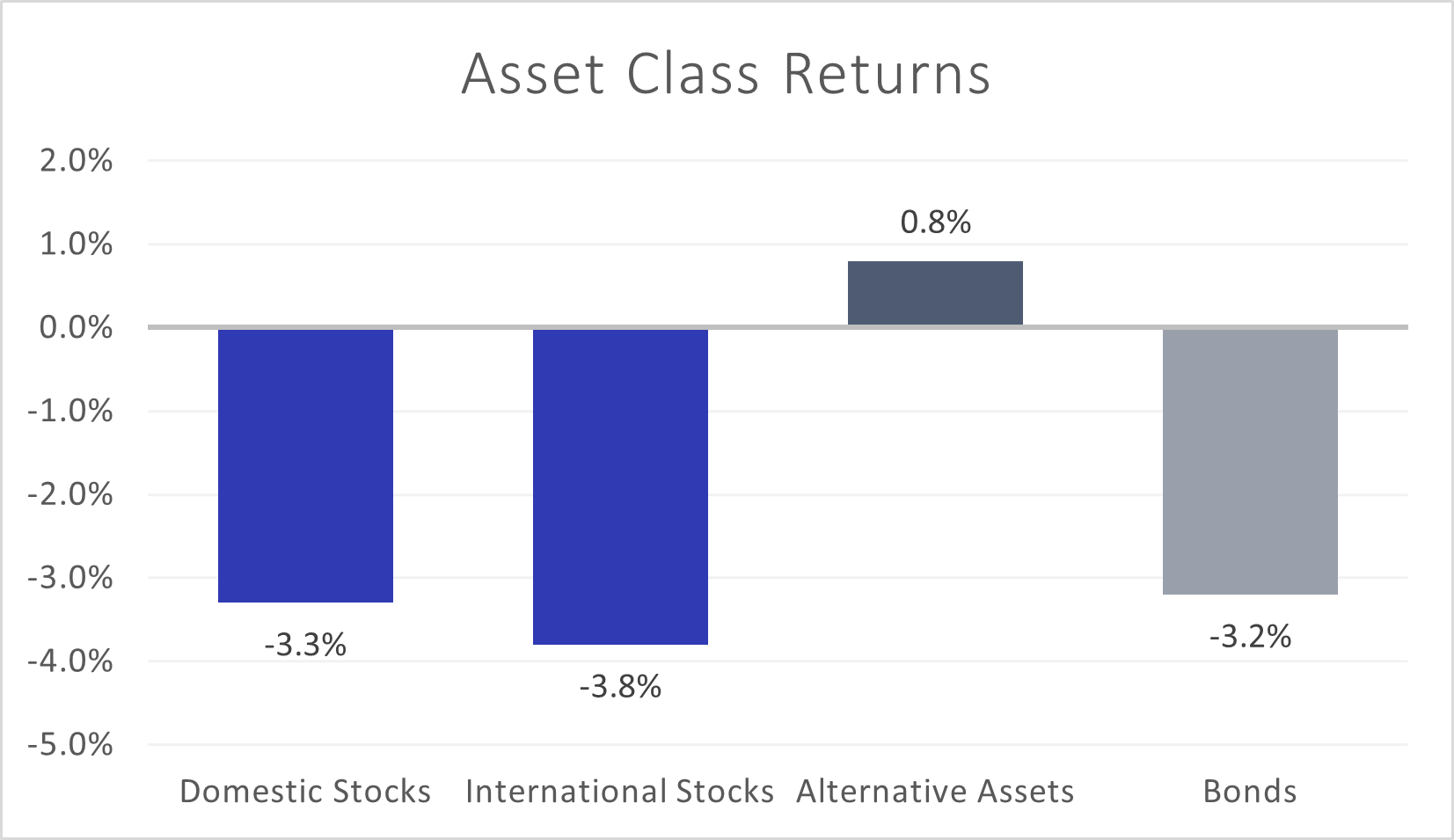

This year’s stock rally stalled a bit in the past three months, as major U.S. indices fluctuated within fairly narrow trading ranges before all finished the quarter lower. While some warning signs have emerged, the recession anticipated in some circles has yet to materialize – as employment, economic growth, and consumer spending data remain supportive to the economy. Large-cap technology company returns continue to outpace other market segments in 2023, leading to relative outperformance by the NASDAQ Composite Index over other broad-based indices. Other asset class performance was mixed, as bond returns remain challenged by escalating interest rates while commodity prices have spiked higher (mainly due to the recent steep increase in oil prices). The yield curve (the difference in interest rates between shorter-dated bonds and longer ones) continues to be sizably inverted, which is clouding the near-term outlook.

Stocks

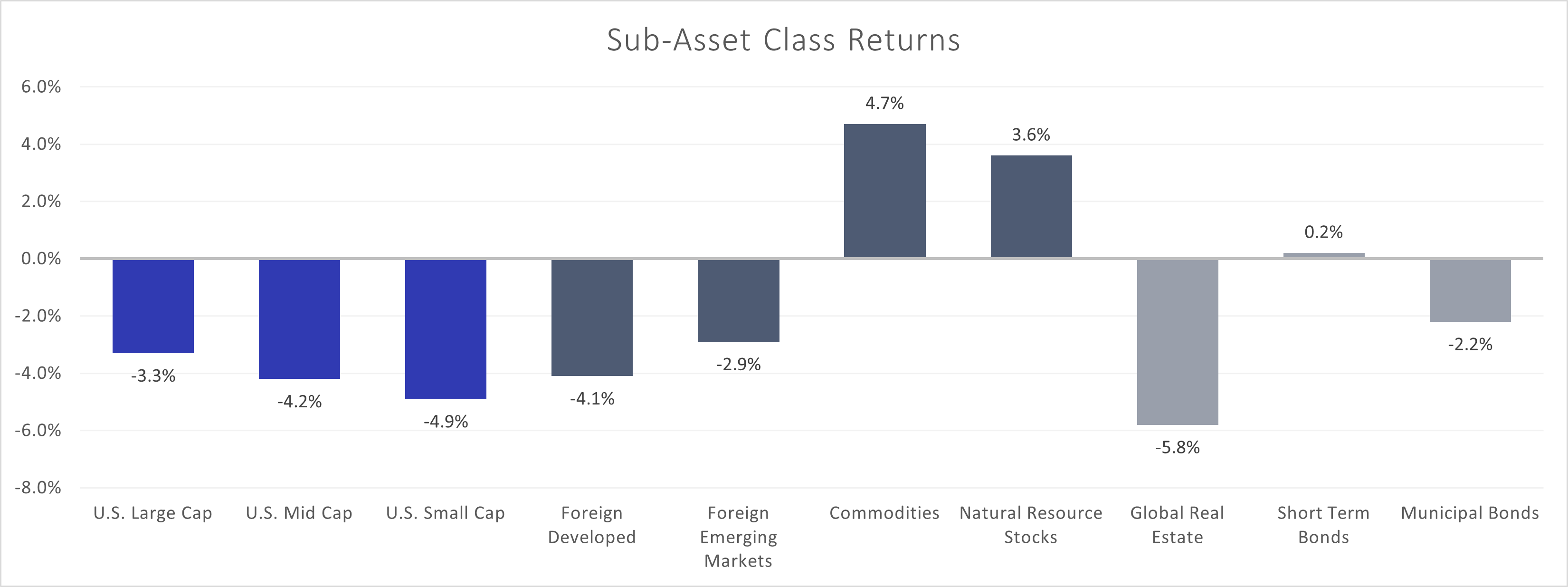

U.S. stocks (Russell 3000) narrowly outpaced the performance of international stocks (MSCI All Country World Index ex-U.S.) in the third quarter, although both finished the quarter lower. U.S. companies continued to post solid earnings; however, the potential for interest rates to move even higher as the Federal Reserve fights inflation weighed down returns in September. Large-sized (S&P 500) U.S. company stocks outperformed their small-sized (S&P SmallCap 600) and mid-sized (S&P MidCap 400) counterparts. Higher Eurozone inflation dampened developed markets (MSCI EAFE) stocks, which underperformed emerging markets (MSCI EM) companies, even as the latter was negatively affected by the economic issues, real estate sector, and manufacturing challenges affecting China.

Bonds

Interest rates continued to edge higher as inflation remained stubbornly elevated, propelling bonds (Bloomberg US Aggregate Bond Index) to post a negative return for the quarter. The yield curve remains sizably negative – a consistent indicator of recession on the horizon, although nothing is etched in stone just yet. As we detail in our Perspective section, future returns for bonds appear more attractive than in years past, due to higher current income payments and potential capital appreciation whenever the Fed hiking cycle ends.

Alternatives

Alternative assets rose in the third quarter, as commodities (Bloomberg Commodity) and natural resources stocks (S&P Global Natural Resources) both gained ground. Oil prices rose substantially through the quarter, heading towards the $100-per-barrel price level seen last August. Global real estate (FTSE EPRA/NAREIT Developed) detracted from overall alternatives performance.

Perspective

“Risk cannot be eliminated, it just gets transferred and spread.” – Howard Marks

Oaktree Capital Management is a leading investment firm specializing in distressed debt securities. Co-founder Howard Marks has been heralded as one of the shrewdest investors of the past 50 years, famous for his “memos” on economics and investing. Marks has built his career around prudent risk management, even though his firm trades in vehicles that are among the most volatile in the financial industry.

Managing risk in investment portfolios is fundamental to achieving financial goals. One of Planning Alternatives’ key tenets is practicing asset allocation when building portfolios for clients. Typically, having exposure to multiple asset classes within an investment strategy results in lower portfolio risk than in a concentrated approach. Stocks and bonds serve as the foundational building blocks of our portfolio construction methodology; while other asset classes may be added where appropriate, stocks and bonds are our starting point. While higher-volatility stocks carry the promise of greater returns, bonds typically serve as a ballast to stock risk, diversifying the portfolio and reducing overall portfolio risk.

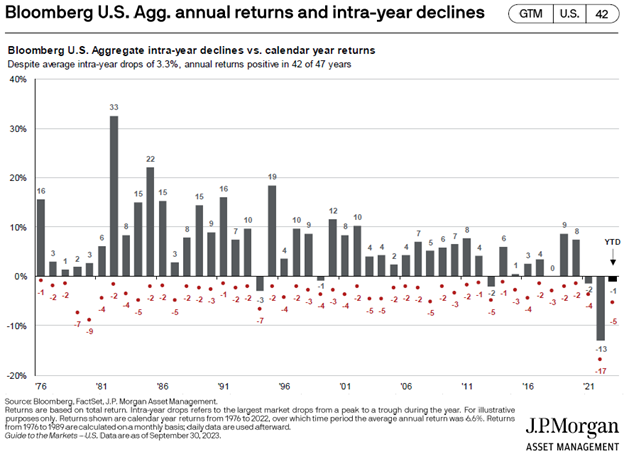

With interest rates rising so dramatically over the past 18 months – rising from virtually zero to their highest level in 22 years – bond returns have been significantly challenged like few times in our recent memory. Why? Because of the inverse relationship between interest rates and prices of existing bonds – as rates have ground higher, prices have fallen. The swift pace at which rates have risen has compounded the effect because fixed income markets have scarcely had enough time to digest one Fed change before another came along. These effects led to a decline in the Bloomberg U.S. Aggregate Bond Index of 13.0% in 2022. Through three quarters in 2023, the index is down another 1.9%. These are not typical bond returns, as evidenced by the last 47 years (see graph below).

Two things stand out: calendar year bond returns (as indicated by the gray bars) have historically been positive while exhibiting low negative volatility (represented by the red dots signifying the largest intra-year drop for bonds). Prior to 2022, even the relatively few times bonds experienced a negative calendar year return, those losses were in the low single-digit range. However, the outlying total return and volatility of 2022 did indeed occur! The aggressive Fed rate hike regime led to the relatively large calendar year decline as prices of existing bonds dropped. At the same time, volatility increased, which caused some investors to question the rationale for including bonds in portfolios at all.

We still feel that bonds are an important component of a successful investing strategy. They help reduce overall portfolio risk and typically serve as a counterbalance in times of stock market declines. Additionally, in the current environment, we think the longer-term future outlook for bonds is the most attractive it has been in at least 15 years. How can this be after we’ve experienced multiple years of challenging returns? The answer lies in the combined nature of measuring total return of bond investments – from both interest payments and capital fluctuation.

Higher rates mean greater interest payments to bondholders, which is additive to total returns. Capital appreciation is trickier to project; however, the most likely path for interest rates over the next several years is lower. This would be beneficial as prices of existing bonds would likely rise in response. Even if the Fed raises short-term rates one more time (as signaled by Fed Chairman Jerome Powell during his September press conference) before halting, the longer-range projection seems likely for rates to decline from current levels. In summary: locking in higher current interest payments, combined with the attractive potential for bond prices to rise as rates decline in the future, in light of the traditional diversification benefits of the asset class, make bonds worth holding.

The largest threat to this thesis would be a broader rekindling of inflation and/or significantly higher GDP growth that would force the Fed to aggressively raise rates further. Although this scenario would boost interest payments of bonds even higher, the corresponding decline in bond prices would likely overshadow those positive interest effects and drive total returns lower.

Positioning

Our belief is that holding bonds serves as the main counter to the risk inherent in stock investing. Rather than try to hit “home runs” with returns in bond investing, our goal is for our bond “sleeve” to modestly outperform the U.S. Aggregate benchmark while improving portfolio risk-adjusted returns via diversification.

The primary way Planning Alternatives accesses fixed income markets is through the use of broadly diversified mutual funds combining exposures to government, corporate, and municipal securities. Mutual funds are for those clients interested in greater liquidity and increased diversification than individual bond investing can offer. Our suite of bond funds includes large positions in core domestic and international managers, supplemented by smaller allocations to managers that have greater flexibility to adjust to market conditions through use of high-yield and other market segments.

Additionally, we offer two separately managed account solutions affording clients greater flexibility and enhanced predictability of outcome that comes with owning a smaller set of individual bonds. The Goldman Sachs Fixed Income Tax Aware SMA utilizes government, corporate and municipal individual bonds in customized portfolios aiming to enhance after-tax yield within taxable accounts. Goldman synthesizes client inputs on tax rates, residency, and credit risk preference to determine the optimal mix, ranging from 100% municipal to 100% corporate (and anywhere in-between) based on what is best for each client’s situation. The account is also fully customizable with regard to credit quality, duration, and maturity.

The Nuveen Intermediate Government/Credit SMA creates individual bond portfolios comprised of both government and corporate issues for tax-deferred accounts (e.g. IRAs). These solutions are fully customizable with regard to credit quality, duration, and maturity. Additional flexibility is available to provide for regular income distributions and ESG considerations.

Please contact your Planning Alternatives advisory team to determine which approach to bond investing is best for your circumstances. Although the short-term path for interest rates is still unclear and could lead to more bond choppiness through the balance of 2023, we believe that the longer-term outlook for the asset class is more appealing than it has been in some time.

Please contact us with questions, or just to chat!