Performance

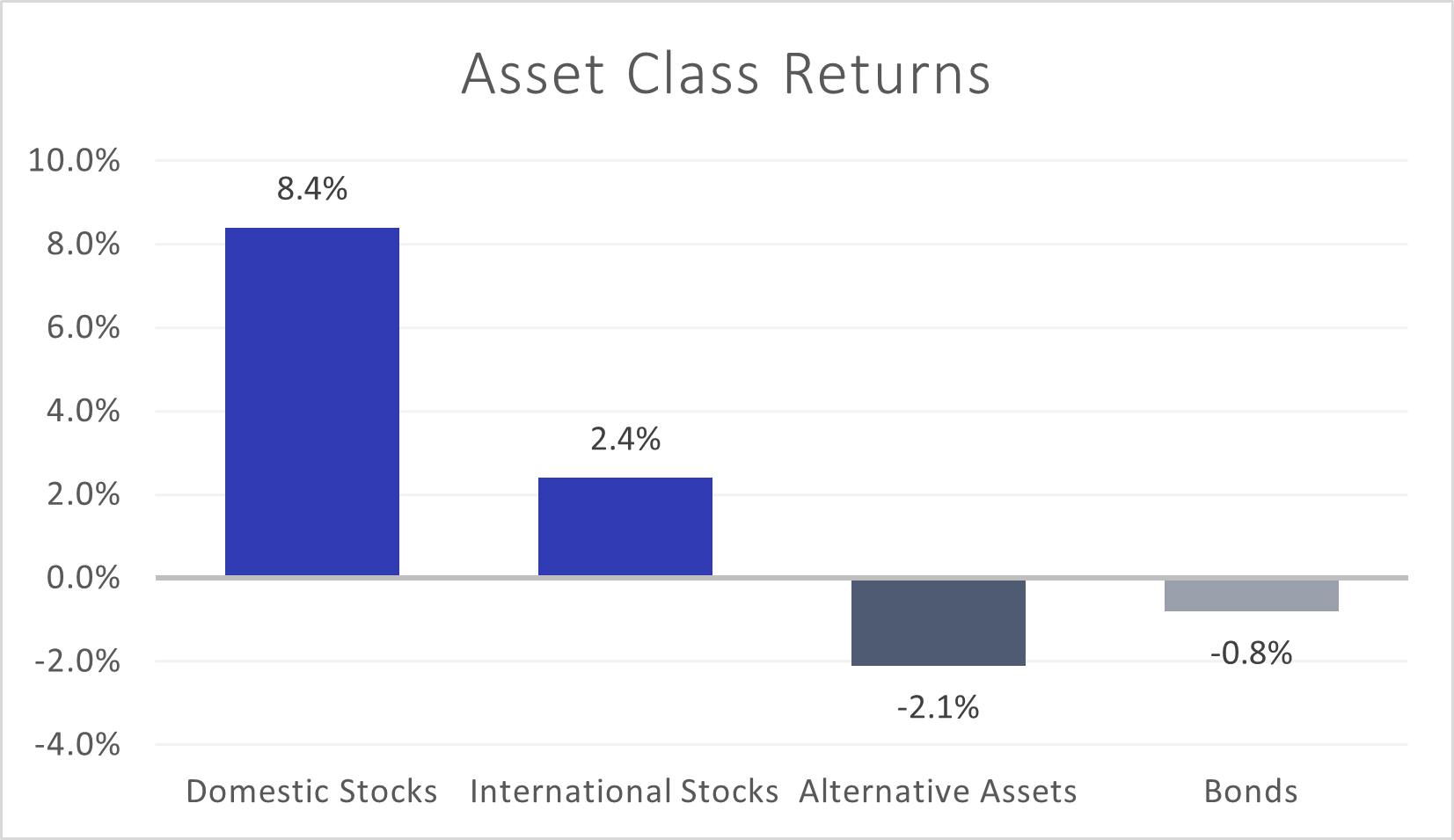

Stocks continued to advance in the second quarter, propelled in great part by shares of large-cap technology companies. Even in the face of increasing interest rates, the U.S. economy has maintained its footing. Corporate earnings continue to be better than expected, the labor market remains strong, and economic growth has yet to precipitously fall off as projected. However, this does not mean that all potential roadblocks have disappeared. Although bonds gave back some of their first-quarter gains as the Federal Reserve continued raising rates, they seem to be well-positioned for the medium-term. Alternative assets continued to decline in the second quarter, led lower by a drop in natural resource stocks.

Stocks

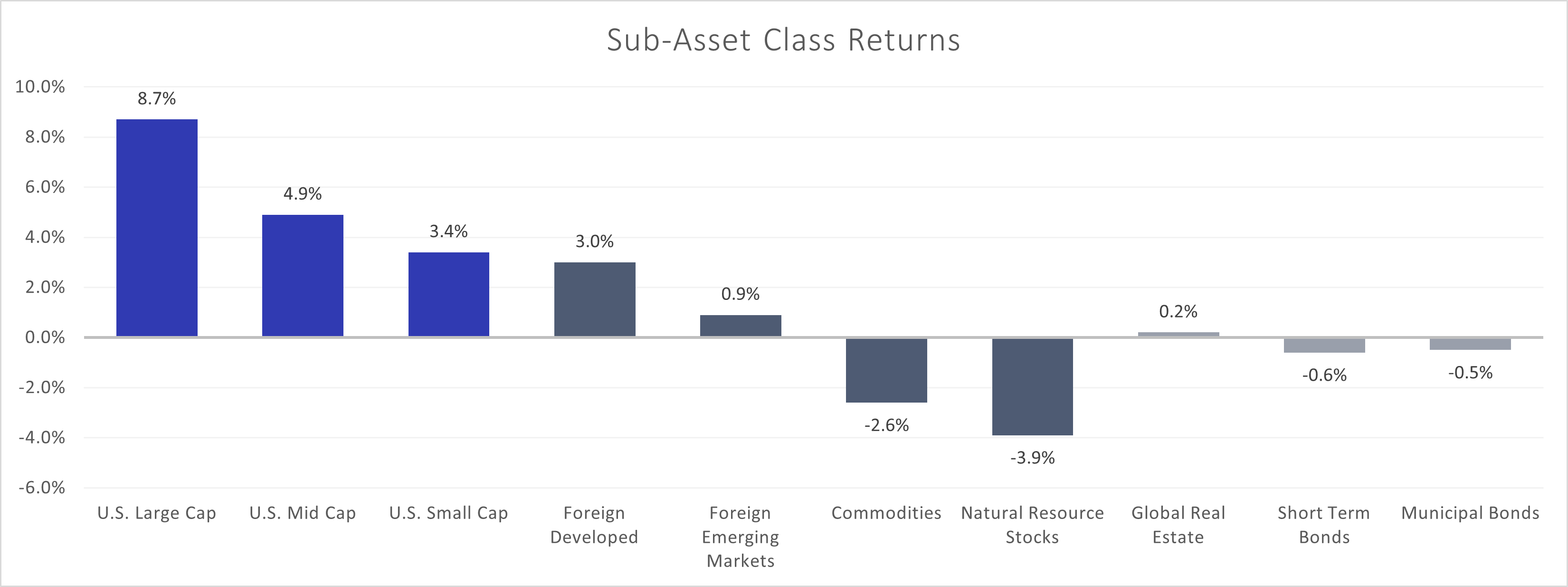

While returns for U.S. stocks (Russell 3000) sizably outpaced those of international stocks (MSCI All Country World Index ex-U.S.) in the second quarter, both still posted strong advances in the first half of 2023. A significant run-up in U.S. mega-cap stocks involved in the artificial intelligence boom guided large-sized (S&P 500) U.S. company outperformance over their small-sized (S&P SmallCap 600) and mid-sized (S&P MidCap 400) counterparts. Overseas, Japanese stocks continued their fast pace in the second quarter, benefitting from lower valuations, a weakening currency making exports more attractive, Chinese geopolitical concerns, and corporate governance rule enhancements by the Tokyo Stock Exchange. This Japanese market strength helped developed markets (MSCI EAFE) stocks to outperform emerging markets (MSCI EM) companies.

Bonds

Bonds (Bloomberg US Aggregate Bond Index) posted a fractional negative return for the quarter. However, the total return outlook for bonds over the next few years is strong; higher income payments combined with the potential for capital appreciation whenever rates decline are reasons for positivity. There are still healthy interest rates available on shorter-term bonds (e.g. Treasuries) that outpace bank checking and savings rates, although this condition may not persist for much longer if the Fed cuts rates over the next six months.

Alternatives

Alternative assets returned negatively over the quarter, predominantly due to weak performance from natural resources stocks (S&P Global Natural Resources) and commodities (Bloomberg Commodity). Global real estate (FTSE EPRA/NAREIT Developed) increased slightly.

Perspective

“One of the funny things about the stock market is that every time one person buys, another sells, and both think they are astute.” – William Feather

The writer and publisher William Feather offered up many homespun quotes over his lifetime, typically full of Main Street sensibility. But his perceptive statement about the simultaneous self-assuredness of both stock buyers and stock sellers was pure gold. While investing is an inexact science full of differing opinions about the future, those contrary views help markets function properly by bringing different opinions together in every trade.

Compelling cases can be made for both a bullish and bearish outlook for stocks over the remainder of 2023. Fundamentally, the resilient strength of the U.S. economy is matched against the most aggressive Federal Reserve interest rate hiking regime of the last 40 years. Which will win out over the next six months? Although stocks have risen significantly over the first half of the year, there are signs that Fed policy has started to dampen the economy – and will eventually lead to recession.

Stocks have demonstrated their durability this year based on a combination of economic surprises and expectations for the future direction of interest rates. Economically: The labor market remains strong, corporate earnings have stabilized, economic growth stayed positive, and consumer spending (the engine that drives more than two-thirds of the U.S. economy) has been remarkably resilient. The expectations game: as stocks are a forward-looking indicator, the belief that the Fed would eventually begin to cut interest rates (with or without the hoped-for “soft landing”) factored significantly into the positive momentum in the first half of 2023.

The major headwind, however, continues to be interest rates – not only their relatively high level compared to the recent past, but the fast pace of the increases. Economist Milton Friedman famously said that monetary policy changes affect economies with “long and variable lags.” That means that when the Fed changes course, reactions in the broader economy are neither instantaneous nor consistent. Short-term rates are so important because they influence the cost of borrowing. Eventually, higher rates curb inflation by stifling demand and slowing down the economy – usually inducing a recession along the way. Follow-on effects of rate policy are becoming more apparent: worldwide manufacturing sector purchasing manager index (PMI) readings have fallen, businesses are signaling cutbacks on capital expenditures, and lending standards have become more stringent in the wake of the banking sector turmoil. If a recession were to materialize, higher lending standards could result in a decline in credit availability to small and medium-size businesses over the next 6-12 months.

The Fed doesn’t have the best track record on slaying inflation without causing recession, but has the pandemic altered this dynamic? Unprecedented amounts of money distributed by the federal government since the spring of 2020 helped fuel a spending surge. While a large portion of that money has been spent, there remains a sizeable amount of cash on the sidelines. Consumer spending on goods and services keeps rolling along, seemingly impervious to the rate hikes over the past year, powering economic growth above expectations. But as pandemic-era savings have run out for some, they fuel consumption via other avenues: the level of credit card debt in the U.S. is approaching $1 trillion. This propping up of consumer spending by the use of credit seems unsustainable over the long term.

Positioning

Two of our core investing tenets are asset allocation and global diversification. The utilization of different asset classes (e.g. stocks and bonds) as well as different geographic regions are hallmarks of our portfolio construction. The majority of our performance can be attributed to the prudent implementation of these two principles; we are not a firm that “bets big” on a single asset class, sector, or region. However, as evidence changes, we seek to capitalize on opportunities and enhance performance by tilting in and out of these categories – resulting in varying degrees of success.

Based on our reading of the economic outlook, we have maintained an underweight position in stocks relative to benchmark weighting through the first half of 2023. While our absolute performance has been solidly positive this year, we have lagged benchmark mainly because of this more defensive position. Markets are exceedingly challenging to forecast even under the most benign circumstances – let alone an environment as conflicted as the current one – but we still believe a slightly more risk-averse position remains the prudent stance to take at this time. On the flip side, our shift of a portion of international stocks to U.S. companies has been additive this year, as has been our decision to replace our core emerging markets exposure with an ex-China fund.

In conjunction with a restructuring of our bond sleeve in May, we took our bond exposure back to benchmark weighting. We feel that the Fed is close to being finished with rate hikes, and that bonds have become more attractive from a total return perspective. Why? Because overall return for bonds is made up of both interest income (which has increased as rates have risen) and capital appreciation potential (which is more attractive given the likely lower path for rates over the next 12-18 months). If there is a significant economic slowdown, bonds could also benefit from money flowing out of stocks.

By the end of the year, we expect that signs of an economic slowdown will be more apparent. We still believe that in order to finally slay inflation, the Fed will be forced to raise short-term rates to a point that is restrictive enough to cause a recession. While the pandemic upset some norms of investing, the old axiom that the Fed will raise rates until they “break something” seems to be the most logical conclusion to the stalemate between a resilient economy and a Fed determined to curb inflation. In our view, it is essential to maintain a diversified approach to portfolio construction, instead of adopting a binary all-in/all-out focus. Given the current landscape, we believe that a slightly defensive position is justified.

Please contact us with questions, or just to chat!