Performance

Asset prices across the board rose over the final three months of the year. Stocks rallied for a sizable portion of the fourth quarter, recouping some of their previous losses for the year. However, the specter of recession drove all major indices lower in 2022, and continues to weigh down the outlook for stocks in 2023. Slowing corporate earnings growth and still-increasing interest rates from the Federal Reserve pose the most significant threat to future stock prices, even as inflation has begun to decline from 40-year highs and unemployment remains near historic lows. Bonds rallied alongside stocks in the fourth quarter; alas, they too could not overcome accrued 2022 losses as the Bloomberg U.S. Aggregate Bond Index suffered its worst year since the index’s inception in 1977. Alternative assets also produced sizable gains in the final quarter of the year.

Stocks

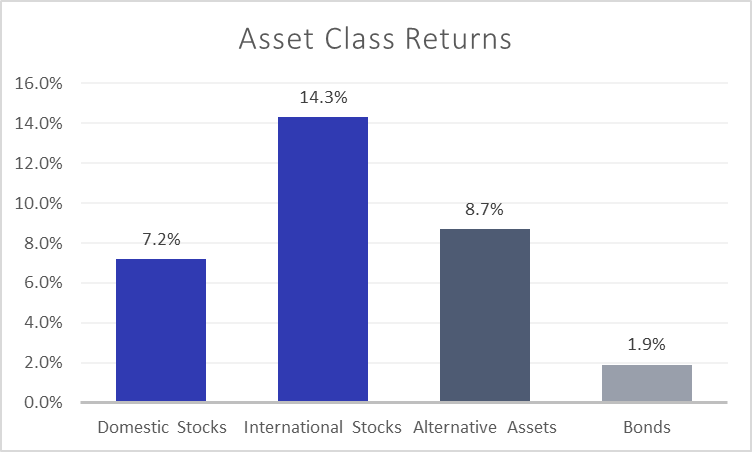

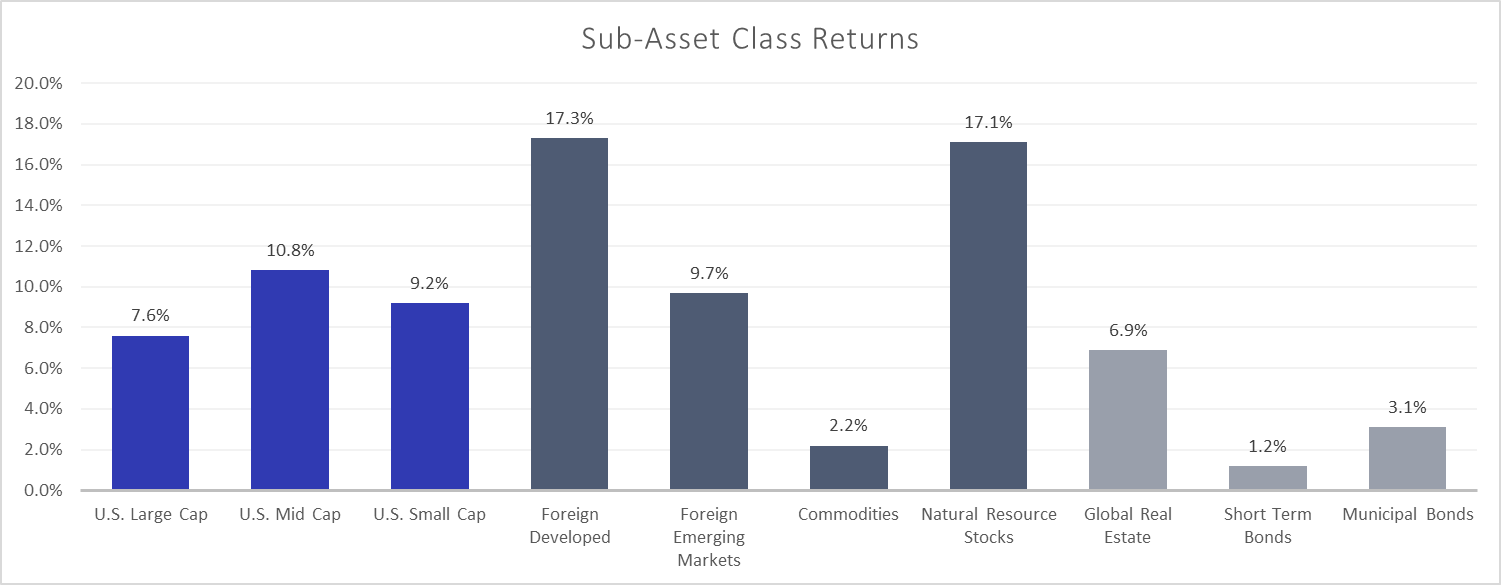

The fourth quarter bump in stock prices was most pronounced outside of America, as international stocks (MSCI All Country World Index ex-U.S.) bettered U.S. stocks (Russell 3000). A decline in the relative strength of the dollar versus foreign currency served as a tailwind to international performance. In addition, foreign stocks remain significantly cheaper than their U.S. counterparts – attracting value investors. However, 2023 prospects in regions such as Europe and China remain challenged by inflation, war, and COVID. On a sub-asset level, international developed markets (MSCI EAFE) stocks again bested emerging market (MSCI EM) companies. Domestically, mid-sized (S&P MidCap 400) and small sized (S&P SmallCap 400) U.S. companies outperformed large sized (S&P 500) ones.

Bonds

Bonds (Bloomberg US Aggregate Bond Index) staged their own rally in the fourth quarter, but (like stocks) finished a long way from overcoming a challenging first three quarters. While higher rates means a higher income return component of bonds, the capital appreciation component of total return remains under duress. Of course, relatively high inflation also hampers bond returns by impairing the purchasing power of interest payments and maturing principal. The silver lining of a challenging 2022 is that future returns for this asset class are much more promising in the coming years due to the relatively low current starting point.

Alternatives

Alternative assets returned 8.7% for the quarter. Natural resources stocks (S&P Global Natural Resources) were up sharply and provided most of the return for the quarter; however, global real estate (FTSE EPRA/NAREIT Developed) and commodities (Bloomberg Commodity) also contributed positively over the three months.

Perspective

“At all times, in all markets, in all parts of the world, the tiniest change in rates changes the value of every financial asset.” – Warren Buffett

We experienced the most aggressive interest rates hiking regime of the last 40 years in 2022, and there were big changes to asset values over the course of the year. Bonds recorded some of their worst returns in history, and stocks staged a roller coaster ride on their path to a substantial decline. 2022 was proof positive that legendary investor Warren Buffett was right when he famously said that interest rates affect everything!

The market’s current obsession is predicting the path of interest rates in 2023, and what it means for the future of asset prices. I believe it’s important to have both a short-term and a longer-term perspective regarding what’s happening in the overall economy. At Planning Alternatives, we typically make portfolio adjustments using a 12-to-18-month outlook. However, when appropriate, we will look to capitalize on shorter-term trends within that broader framework. Let’s examine our current views for each of these a little closer:

In the first half of 2023, our expectation is that the U.S. will be in a pronounced economic slowdown. We feel that a recession is fairly likely within this timeframe. Even if we avoid recession, stocks prices likely will retreat further from current levels in anticipation of one. While not the sole arbiter of recession, current estimates for 2023 U.S. GDP growth, which range from 0% to 1%, are not very promising. It’s possible that the first half of the year will see negative GDP growth, but that we work our way toward those projections by the end of the year. Inflation figures, unemployment trends, and interest rate decisions from the Federal Reserve will once again inform returns – especially over the first 6 months of the year.

The opinion that things will likely get worse before getting better is also predicated on the belief that inflation will continue to fall, but take much longer to get anywhere close to the Federal Reserve’s target of 2%. Stubbornly elevated Inflation would precipitate more hikes than the widely anticipated two (in February and March) before the Fed is finished raising rates. The old adage of “Don’t fight the Fed” bears attention; as long as the Fed continues to aggressively raise rates to combat inflation, asset returns will continue to be challenged.

Even if we experience a recession during 2023, I don’t anticipate it will approach the severity of 2007-2008. Businesses and consumers are much better positioned, with lower debt levels and higher savings levels. Further, the fact that upwards of two million people have retired from the workforce since the onset of the pandemic has made companies more reluctant to lay off the workers they still have. Of course, the possibility of a more substantial economic downturn could materialize in 2023 – particularly if corporate profits drop more than expected, inflation doesn’t fall as quickly as hoped, and the Fed keeps hiking rates through the spring and summer.

The silver lining of the decline in stock and bond prices in 2022 is that the longer- term outlook for both asset classes looks more attractive than it has in the past several years. Why? As bond yields have increased sharply, investors are receiving more interest for the same principal amount. This, combined with the potential for interest rates to begin declining sometime over the next 12-18 months (existing bond prices move inversely with interest rates), means that total returns for bond investments could be poised for an upswing. Similarly, stocks are more reasonably valued than last January – unfortunately, that’s what a sizeable downturn in the S&P 500 Index brings! This means that forward returns from the current starting point are more promising than they were at the start of 2022 because stock investors now are paying substantially less per unit of corporate earnings (i.e. a lower P/E ratio).

Positioning

After moving in June 2022 to a neutral stock positioning relative to our benchmark weighting, our investment committee deliberated long and hard about our next move as we dissected voluminous economic and market data. Results from the fourth quarter rewarded our patience, as stocks rode a bumpy path eventually higher over the quarter.

As outlined in the Perspective section, our base expectation is that the U.S. economy will slow in 2023 before it improves, largely due to the demand softening brought on by the Fed’s aggressive interest rate tightening. Anticipation of this partially led to the decline in stock prices in 2022; however, we feel another leg downward in stocks is likely during the first half of 2023, as the Fed keeps raising rates and corporate earnings come under more pressure. As a result, we made some portfolio adjustments at the end of the year. First, we felt it was prudent to downshift our stock exposure to underweight benchmark. This was done on a relative basis; for example, a 50% benchmark stock portfolio will now have 46% in stocks (i.e. 8% relative decrease). For now, we’re holding proceeds in money market accounts to earn an attractive yield without significant principal risk. Although bonds are also currently attractive, we prefer to hold off on an additional allocation until a potentially better entry point accompanies clear indications that the Fed is closer to ending the rate hikes.

Additionally, we adjusted our overall stock mixture to slightly reduce our international exposure in favor of U.S. companies. At the same time, we replaced our indexed emerging markets ETF (which included Chinese stocks) with a different fund (Columbia Threadneedle EM Core ex-China: ticker XCEM) that does not include China exposure. China’s current struggles with COVID and economic growth, along with questions about the veracity of economic and health data disseminated from the Chinese government led to this decision. We have the ability to add Chinese stock exposure back later if conditions warrant; however, ongoing tensions with the U.S. and a developing trend of “reshoring” manufacturing to America from China are potential longer-term headwinds for Chinese stocks.

Overall, after a period of unease in the first half of the year, we feel there will be a more opportune time to add stock exposure later in 2023. When there is more economic clarity and/or a more compelling entry point for stocks, we will not hesitate to act. While a recession is possible, it is not inevitable. Even if one does occur, we feel that it will not be overwhelmingly severe – leading to an opportunity for riskier assets such as stocks and lower credit quality bonds to bounce back in the second half of the year.

We wish everyone a peaceful and healthy 2023. Please contact us with questions, or just to chat!