Performance

Following the trend of the tumultuous first half of the year, U.S. stocks moved lower in the third quarter. International stocks also fell; developed markets and emerging markets both posted losses as Europe contends with energy and economic growth concerns, and COVID lockdowns complicate China’s economic recovery. Inflation showed some signs of having peaked; however, Federal Reserve interest rate policy will likely stay aggressive as long as the absolute level remains well above the Fed’s 2% target. Inflation and rising interest rates stymied bond returns; this double whammy has prevented bonds from cushioning against 2022 stock losses. Alternative assets did not fare any better, with commodities, real estate and natural resources all coming under pressure.

Stocks

On a relative basis, U.S. stocks (Russell 3000) regained the upper hand on international stocks (MSCI All Country World Index ex-U.S.) in the third quarter. U.S. stocks were boosted in July and August (before dropping again in September) by the view that the Federal Reserve will slow or stop short-term interest rate hikes in 2023. International stocks were hampered by warfare and energy problems in Europe, as well as by continuing COVID lockdowns in China, which affected goods production, shipping, and manufacturing. Mid-sized (S&P MidCap 400) U.S. companies outperformed their large-sized (S&P 500) and small-sized (S&P SmallCap 600) company counterparts. The leadership position in overseas stocks flipped, resulting in developed markets (MSCI EAFE) stocks besting emerging markets (MSCI EM) companies.

Bonds

Bonds (Barclays U.S. Aggregate Index) still could not overcome the dual headwinds of stubbornly high inflation and higher interest rates, posting a third consecutive quarterly loss. The two most-followed regular news events remain the monthly CPI inflation data release and any time Federal Reserve Chairman Jerome Powell speaks publicly; markets remain fixated on any clue as to when inflation and rates might be poised to trend downward. Across the entire fixed income spectrum, shorter duration funds fared best in the rising rate environment.

Alternatives

Alternative assets declined 6.8% for the quarter. Natural resources stocks (S&P Global Natural Resources), global real estate (FTSE EPRA/NAREIT Developed), and commodities (Bloomberg Commodity) all contributed negatively over the three months.

Perspective

“Don’t fight the Fed.” – Martin Zweig

Most of the market gyrations this year can be traced to the tug-of-war between inflation and the associated Federal Reserve response to tame it. Will the Fed end up inducing a recession to finally slay inflation? That remains the key question. Seemingly every day, I find myself scanning the news to glean the very latest updates on inflation and what the Fed is trying to do in order to tame it. While most people who don’t work in the financial industry have more exciting things to do than track every utterance of Jerome Powell, it is important to understand why inflation and the Fed response are so determinative to stock and bond prices.

The late economist Milton Friedman characterized inflation as “too much money is chasing after too few goods.” Pandemic-induced supply-and-demand imbalances, an overwhelming amount of government spending in response to closing down the economy, and ultra-low interest rates had elevated inflation even before the Russian invasion of Ukraine in the beginning of 2022. The war exacerbated pricing imbalances and the Fed’s delay in raising short-term interest rates and turning off the spigot of bond-buying helped to entrench inflation at the high levels that persist today.

Even though the market expected the pace of decline to be more significant, August’s 8.3% increase in the year-over-year inflation rate indeed marked an improvement over July’s 8.5% increase. Looking beyond the top-line figure, there is some evidence that inflation could remain more stubbornly high than the Fed hopes. So-called “flexible” (faster changing) components like food, fuel, vehicles, and hotel costs have fallen in the aggregate this year. However, “sticky” (slower to change) components such as shelter, healthcare, and public transportation have seen an uptick in 2022. If sticky inflation rises or remains at current elevated levels, the Fed’s task to reduce inflation anywhere near its 2% target (or even the long-run average of 3.5%) becomes even more difficult, particularly if flexible inflation rises in any meaningful way.

High inflation can affect stock prices in several ways. Higher raw material prices can increase business costs, reducing profit margins and earnings. Demand for goods and services can fall due to higher prices, also affecting revenue and earnings. Most importantly, the Fed typically raises short-term interest rates to reduce inflation; if this happens too quickly or goes on for too long, it can ultimately induce recession to bring demand back into phase with supply.

Bond prices are hampered by inflation in two main ways. First, interest payments lose purchasing power over the length of bond; second, as the Fed raises rates, this can decrease the value of existing bonds. However, the silver lining of rising rates is that bond income typically rises at the same time. Because the total return of bond investments combines income and price fluctuation, additional income helps to offset price declines.

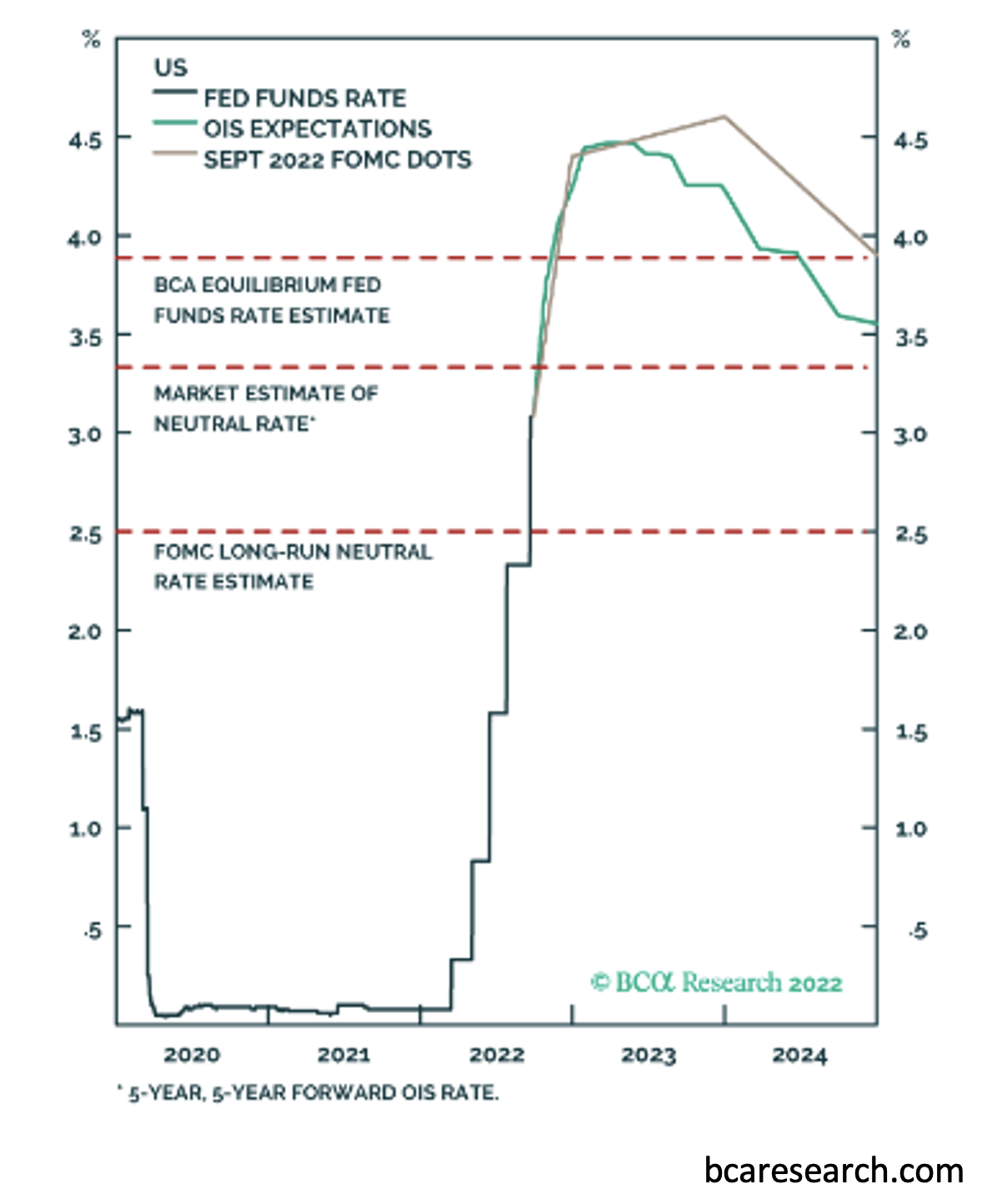

Markets are hoping the Fed can manage to pull off a “soft landing” of taming inflation while avoiding recession. The recent summer rebound in stock prices was predicated on the belief that the Fed will stop raising (and eventually cut) rates in 2023 (green “OIS Expectations” in the below chart). However, this expectation is contrary to the future estimates of the Fed via its “dot plot,” which summarizes the short-term interest rate projections of Fed members (gray “Sept 2022 FOMC Dots).

What’s going to happen in 2023? Our expectation is that inflation will ease somewhat as supply chains continue to heal and the Fed’s rate hikes clamp down on demand, but it is going to be very challenging for the annual inflation rate to approach the 2% target next year. Chairman Jerome Powell remains consistent in his rhetoric about doing what is necessary to slay the inflation dragon, regardless of the challenges that would result. “Higher interest rates, slower growth and a softening labor market are all painful to the public that we serve. But they’re not as painful as failing to restore price stability and having to come back and do it down the road again,” he stated during his September 21st press conference announcing another 0.75% short term rate hike. As a result of the Fed’s steadfastness, it is becoming more and more likely that a recession resulting from Fed rate hikes will be required to break the back of inflation at some point in the next 12 months. Although stocks could certainly move lower from here, we feel that the negative performance of this year has already largely baked this eventuality into stock prices.

Positioning

This summer, once it became apparent that the Fed was embarking on an interest rate tightening cycle to clamp down on inflation, we throttled back on stock exposure and held proceeds in money market funds. In the midst of rising rates, we were cautious on adding to bonds. Markets have whipsawed since our June trade – staging a rally in July and August before retracing to new yearly lows in September.

So what may lie ahead for financial markets? Consumer spending, employment, and corporate and consumer savings levels remain quite strong. If year-over-year inflation moves downward more substantially, there is potential for a rebound through the end of the year and into the start of next year. Given the absence of a clear short-term direction, a neutral allocation remains prudent. However, we are examining the nuances of each inflation report and Fed press conference to inform our future decisions on asset class allocations.

In the meantime, our current mixture of stock funds reflects our emphasis on certain market sectors. This focus has been additive this year, as our JP Morgan Diversified Return U.S. Equity fund (JPUS) emphasizing metrics such as value, momentum and quality along with our Vanguard Dividend Appreciation fund (VIG) highlighting companies that consistently return cash to shareholders via dividends are both outperforming our U.S. benchmark (Russell 3000 Index). These funds don’t have quite as much emphasis on large-cap tech stocks, which have been most negatively affected by the inflation and rising rate environment. Additionally, our actively managed Goldman Sachs / GQG Partners international stock fund has bested our international benchmark (MSCI ACWI Ex-U.S. Index) year to date.

Given this year’s uncommon simultaneous drop in stock and bond prices, after careful consideration we recently approved several new investment products to complement our existing suite of funds, individual holdings, and separately managed accounts. We are working with two leaders in multifamily and industrial real estate – Blackstone and Starwood – on products that offer sources of income and return that enhance diversification by not moving in lockstep with stocks and bonds. Additionally, we have two new fixed income offerings – a bond ladder and a bond separately managed account – that can help to mitigate the various risks of fixed income investing. These strategies provide both increased predictability of outcome and greater tax flexibility than traditional mutual funds. With a focus on holding individual bonds to maturity, these solutions can help reduce some of the risk a rising interest rate environment poses for fixed income investing.

All of these newly introduced strategies may not be appropriate in every circumstance, so please review with your advisory team to assess if they could be beneficial for you.

Please contact us with any and all questions. We are always here to help!