Performance

Concerns about slowing global GDP growth and higher COVID-19 delta variant infections weighed on stock returns this quarter. The combination of these effects spurred a rotation from sectors that thrived in the first half of the year (small-cap U.S., value, and emerging markets stocks) to large-cap U.S. and developed international stocks. Inflation stayed elevated, although leading contributors such as used cars, hotel and airfare prices began to reverse from their highs. Bonds inched upwards even as longer-term interest rates experienced volatility. Alternative assets gained in the third quarter, although some commodity prices began to normalize.

Stocks

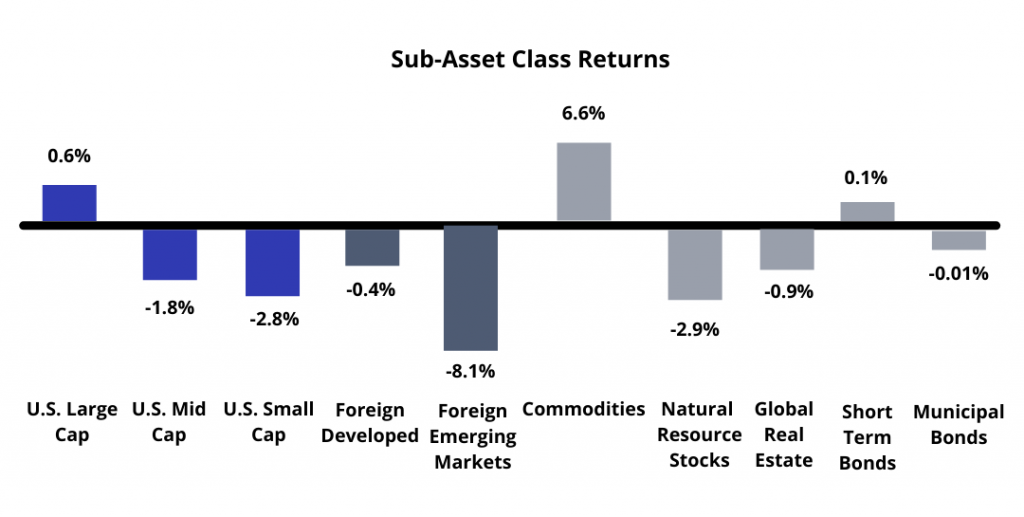

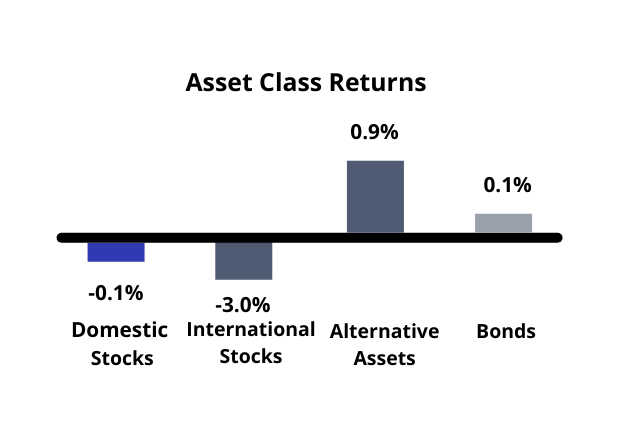

U.S. stocks (Russell 3000) fell 0.1% over the quarter, outpacing the 3.0% loss of international stocks (MSCI All Country World Index ex-U.S.). The flight to relatively safer options led large-sized (S&P 500) U.S. companies higher, as they bested small-sized (S&P SmallCap 600) and mid-sized (S&P MidCap 400) companies. Overseas, developed markets (MSCI EAFE) bettered returns from emerging markets (MSCI EM); the resurgence of the COVID-19 delta variant seemed to affect lower-vaccinated emerging countries more than developed nations. Additionally, the Chinese regulatory crackdown on several key industries weighed on emerging markets returns.

Bonds

Longer-term interest rates fell to open the third quarter, before rising essentially back to where they started. Bonds (Barclays US Aggregate index) were up 0.1% during the quarter. Federal Reserve Chairman Jerome Powell walked the tightrope regarding future monetary policy; most observers took his most recent comments to mean that tapering of bond purchases will begin late in 2021 – leaving the door open for short term interest rate hikes to being in late 2022 or early 2023.

Alternatives

Supply and demand imbalances continue to plague worldwide raw materials markets; seemingly just as some commodity spot prices fall from pandemic highs, others spike up. Overall, alternative assets rose 0.9% for the quarter, with a positive contribution from commodities (Bloomberg Commodity) overcoming the negative performance of natural resources (S&P Global Natural Resources) and global real estate (FTSE EPRA/NAREIT Developed).

Perspective

“Life is full of challenges, but I always have the Three Ps: Passion, patience, and persistence. And the fourth one is pizza.” – Butch Hartman

If only more pizza could solve our pandemic-induced health, economic, and political challenges – how quickly we would have skated past this historically crazy time! Although not as tasty as pizza, our utilization of the three other Ps mentioned is the recipe for methodically working through the (hopefully!) end stages of the pandemic.

Looking back, it is truly remarkable how far we’ve come since the dark days of March 2020. A historic effort to research, develop, manufacture, and distribute multiple vaccines to combat COVID-19 came to fruition – with over 400 million shots administered in the U.S. and over 6.5 billion worldwide. The tireless dedication of health care professionals has been demonstrated time and again through their compassionate caregiving. Although delta variant case numbers have spiked (and further mutations are inevitable), mortality rates will likely drift lower due to the effectiveness of vaccines against serious symptoms and death.

The bounce back in stock prices has been almost as impressive as the vaccine effort. It’s important to remember that the stock market is not equivalent to the economy – but it is a forward-looking barometer of economic expectations. The doubling of the S&P 500 Index over the past 18 months was due in part to expectations for a sharp recovery once the worst of the pandemic was over. Economically, the rebound in corporate earnings has been impressive and unprecedented monetary and fiscal policy stoked a recovery in demand from consumers. However, the virus and its aftermath continue to cloud several fronts of the economic landscape.

Economic growth: After ramping up last fall and accelerating into this past spring, GDP growth may have crested, although still elevated when compared to last year. Economic output naturally blazed higher as countries reopened across the globe; the challenge is divining how long the elevated output will last.

Inflation: Supply chain shortages and logistical bottlenecks continue to plague everything from automobile production to oceanic shipments of consumer goods. Recent data suggests that the rate of increase of inflation has eased, mainly due to easing in prices of the main contributors – new and used vehicles, airfare, hotel and rental cars. The effects of a global shutdown of economic activity on prices will be felt until at least 2022 – although different industries will be affected at different times. Will higher Inflation be transitory or persistent?

Employment: Unemployment claims and the unemployment rate have both retreated from pandemic highs, but remain elevated relative to pre-pandemic levels. Enhanced unemployment benefits ended in September, but any effects will take time to show in the data. It’s possible that the collective American workforce will never be the same: many workers opted for early retirement during the pandemic, while others left corporate life to start their own companies. How will the Federal Reserve interpret the employment data in making decisions on monetary policy?

Interest rates: Short-term interest rates remain near zero, and the Fed will likely keep them there until at least late 2022. Tapering of bond purchases is likely to begin late this year or early next year –potentially causing volatility in stock markets. How will the Fed balance the need to move to a more normal interest rate policy against this potential volatility?

Fiscal policy: As a nation, the U.S. has spent $6 trillion to combat the pandemic – more than for all of World War II (adjusted for inflation). To what extent (if any) additional spending is necessary is a bitterly debated issue in Washington – additional spending legislation originally thought to be a slam-dunk has the potential to bog down as proposal details are worked out. Is additional spending necessary to continue stimulating the economy, or would it just burden us with more unsustainable debt?

Positioning

Portfolio managers must sift through available data, attempt to read the tea leaves on the future, and adjust portfolios accordingly to their views. Two hallmark tenets that guide our portfolio construction are asset allocation and global diversification. To complement these core principles, we utilize tilts to express our opinions for the future.

We typically make adjustments based on trends we believe will last 6-12 months, rather than react to shorter-term noise. We are continuing our slight overweight to stocks relative to bonds, mostly from our beliefs that corporate profits will remain strong and that stocks are slightly less expensive than bonds. We slightly reduced our exposure to emerging markets – a move that may only be necessary for a few months, an exception to our normal time horizon due to extensive COVID-19 effects in lesser-vaccinated emerging countries as well as the recent Chinese regulatory crackdown – and made a modest allocation to a U.S. large-cap growth fund. We believe this allocation will serve as a ballast if economic growth and inflation have peaked, or if COVID effects linger through the fall and winter months.

Our opinion remains that inflation will not pose a longer-term threat. However, in the short term, massive supply chain disruptions – shifting consumer demand, skyrocketing shipping costs, inventory shortages – will continue to wreak havoc with prices. We anticipate it taking until at least first quarter 2022 for the imbalances to correct. After the Federal Reserve begins to taper asset purchases in late 2021 or early 2022, we think they will wait to see significant gains and increased stability in the labor market before adjusting rates upward – even if inflation remains elevated.

A final note, we anticipate that returns for major asset classes over the next several years will be more muted. A return to slower economic growth seems likely, and since the gains of the last year are not sustainable, it’s reasonable to expect more diminished stock performance. Additionally, bond returns face challenges over the coming years as interest rates return to normal. Staying true to core principles – asset allocation and diversification – while remaining open to the potential for non-traditional asset classes will be paramount over the coming years.

Please contact us with questions, or just to chat!