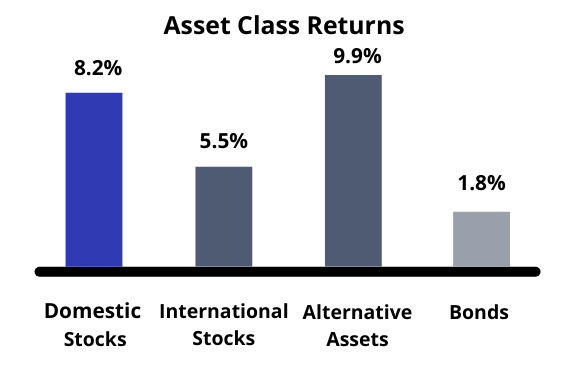

PERFORMANCE

Sparked by accelerating economic growth and a worldwide COVID-19 vaccination effort gaining steam, all major asset classes advanced in the second quarter. Inflation spiked in the second quarter, resulting from several factors: comparisons to last year’s pandemic depths, supply and demand imbalances, and consumers signaling their improving confidence via increased spending on the services sector of the economy. Commodity prices rose, helping alternative assets to performance leadership for the quarter. Bonds recovered a portion of their first quarter decline as interest rates retreated somewhat from their first quarter highs.

STOCKS

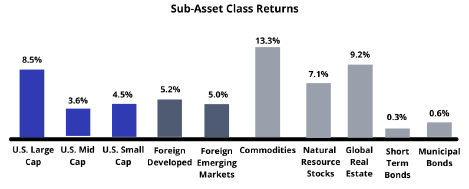

Stocks in all regions climbed higher in the second quarter. U.S. stocks (Russell 3000) returned 8.2% for the quarter, outpacing the 5.5% return of International stocks (MSCI All Country World Index ex-U.S.). Large-sized (S&P 500) U.S. companies outperformed their small-sized (S&P SmallCap 600) and mid-sized (S&P MidCap 400) counterparts, even as all three categories continued their strong 2021 performance. Overseas, developed markets (MSCI EAFE) bettered returns from emerging markets (MSCI EM) on a relative basis.

BONDS

Longer-term interest rates fell from their first quarter highs; in response, bonds (Barclays U.S. Aggregate index) rose 1.8% during the quarter (typically, there is an inverse relationship between interest rates and existing bond prices). The Federal Reserve signaled that short-term interest rates would likely remain near zero through 2022, while leaving the door open to multiple rate hikes in 2023. While not our baseline expectation, the possibility of higher, persistent inflation remains a threat to future fixed income returns.

ALTERNATIVES

Most raw materials prices rose during the second quarter; commodities from oil to lumber to copper moved higher. As supply and demand moved back towards balance, some spot prices retreated from their highs; still, commodities (Bloomberg Commodity) was the alternative category’s leading performer. Overall, alternative assets rose 9.9% for the quarter, with contributions from global real estate (FTSE EPRA/NAREIT Developed) and natural resources (S&P Global Natural Resources), which also gained as economic demand strengthened.

PERSPECTIVE

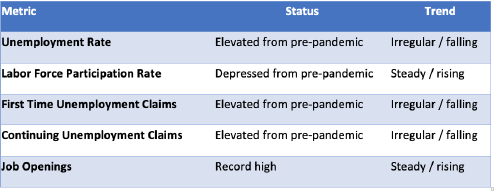

Arguably, the pandemic disrupted the labor market more than any other facet of the American economy. Think back to January 2020: record low unemployment levels in the U.S. and expectations for continued full employment. While it is easy to understand why employment dropped off a cliff last spring – a shutdown of the U.S. economy! –the path forward is murkier.

So many facts, figures, and statistics go into describing this sector that it is sometimes challenging to keep everything straight. Summarized below are some key labor market metrics along with their current status and directional trend:

Labor force participation rate, defined as the percentage of civilian population 16 and older that is working or actively looking for work, serves as an important measure of the available workforce at any given time. After so many discouraged workers left the workforce entirely during the pandemic, it is crucial that this number returns at least pre-pandemic levels.

After more than 22 million workers lose their jobs at the start of the pandemic, we have seen a slow but steady return to work as the economy has reopened. U.S. employers have brought millions back to work; however, there remains a record 9.3 million job openings. Why? One opinion is that the enhanced unemployment benefits extended through September 2021 via the most recent legislation signed into law by President Biden are to blame for the persistently high numbers. By paying benefits recipients their standard unemployment amount, plus an additional $300 per week, many argue that this provides a disincentive to work for those earning more to remain idle. Another opinion is that childcare logistical challenges and COVID health concerns are keeping workers from seeking employment. Whatever individuals’ reasons, the fact remains that workers are proving very difficult to find at the precise time when many companies need them.

Why is employment so important to understanding the economy and markets? Aside from the obvious effect of more people working equaling more economic output, the answer resides with the Federal Reserve, whose stated goals are price stability (i.e. inflation around a certain target) and maximum sustainable employment. While prices have fluctuated based over the past year due to supply/demand imbalances as well as extensive fiscal stimulus, longer-lasting inflation generally requires a broad level of wage increases that results from full employment in a growing economy. When these conditions are present, the Fed starts raising interest rates – which in turn can cause stock market volatility.

Based on the decline in the labor force participation rate, the increase in the unemployment rate, the still-elevated number of first-time and continuing unemployment claims, and the record number of job openings – we still have a long way to go. Once the unemployment rate falls, and businesses are competing (in the form of higher salaries) for workers, increasing wages will likely be the catalyst for Fed action.

POSITIONING

Our investment philosophy continues to be guided by our company’s four key tenets: asset allocation, global diversification, cost sensitivity, and marrying portfolios to a financial plan. The current state of employment, and the Federal Reserve’s interpretation of the data, helps to inform our opinion about which investments are currently most appropriate, while always practicing a discipline of risk management.

We expect that throughout the remainder of 2021, employment metrics will improve, economic growth will remain strong, and that inflation will fluctuate up and down as supply chains work their way back to normal. However, we feel this combination of factors will not be significant enough to force the Fed into meaningfully altering their game plan of tapering bond purchases beginning in late 2021 / early 2022 and beginning short-term interest rate hikes in late 2022 or early 2023.

We continue to favor stocks over bonds on a relative basis; earlier this year we effected a 5% reduction in bond exposure in favor of stocks. The post-pandemic combination of GDP growth, corporate earnings growth, and continued central bank low interest rate policy has been positive for stocks and likely will be through the end of the year. Although obstacles remain before the pandemic can be declared over, especially within the labor market, we are confident in our current investment positioning.

However, close attention and analysis will be required for 2022 and beyond. The interplay between employment, interest rates, and the Federal Reserve will be superimposed on a background of stretched stock and bond valuations. Return expectations may need to be adjusted downward, and flexibility in search of opportunities will be necessary. We are ready for the challenge.

Please contact us with questions, or just to chat!

Jim Long, CFA, CFP®, CMFC®

Director of Investments

You can follow us on YouTube, LinkedIn, Facebook and Twitter.