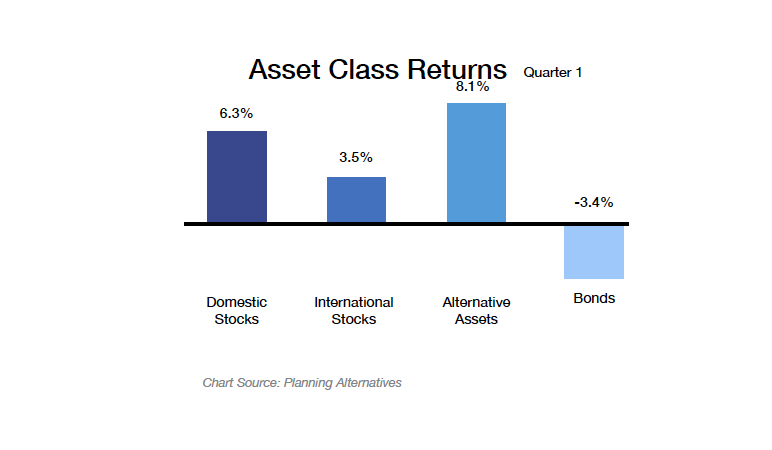

PERFORMANCE

Stocks marched upwards in the first quarter of 2021, driven higher by improving corporate earnings and the hope that the vaccination effort will lead to significant economic growth in the second half of the year. Major U.S. stock indices all touched new record highs in March, led by small and mid-cap stock performance. Bonds suffered a loss in the quarter as longer-term interest rates rose. Alternative assets performed strongly as natural resource and commodity prices continued to recover.

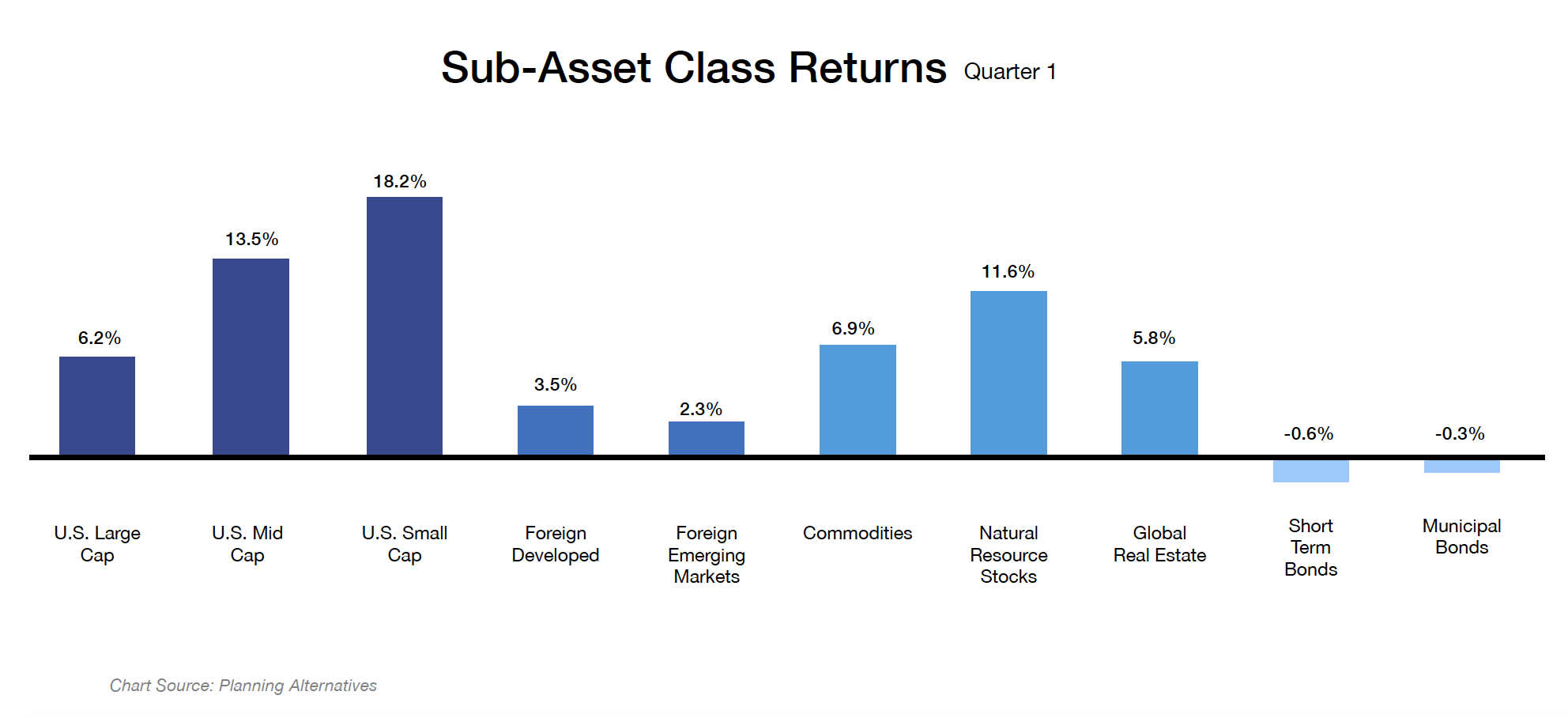

STOCKS

U.S. stocks continue to benefit from an improving economic situation and more widespread vaccination against the coronavirus. The positive momentum of small-sized (S&P SmallCap 600) and mid-sized (S&P MidCap 400) companies sustained a trend that began last fall, as their returns widely outpaced large-sized (S&P 500) companies. Overall, U.S. stocks (Russell 3000) were up 6.3% for the quarter. Remarkably, the Russell 3000 has gained more than 89% since falling to a pandemic low on March 23, 2020.

International stocks (MSCI All Country World Index ex-U.S.) achieved positive returns over the first quarter, gaining 3.5% to finish slightly behind their U.S. counterparts. Developed markets (MSCI EAFE) bettered returns from emerging markets (MSCI EM) on a relative basis.

BONDS

Bonds (Barclays U.S. Aggregate Index) fell 3.4% during the quarter. Longer-term interest rates rose sharply in February and March as investors grew more comfortable with the economic growth outlook, even as the Federal Reserve affirmed its commitment to keeping short-term rates near zero for the foreseeable future. The year 2020 was a remarkably good one for bond performance, considering the economic calamity caused by the pandemic. Bond returns will likely be challenged this year, as the recovering economy exerts upward pressure on interest rates.

ALTERNATIVES

Natural resources (S&P Global Natural Resources) again led the alternative asset category’s quarterly performance. Simultaneously, global real estate (FTSE EPRA/NAREIT Developed) and commodities (Bloomberg Commodity) also rose along with economic growth expectations. Overall, alternative assets rose 8.1% for the quarter.

PERSPECTIVE

“Inflation is when you pay fifteen dollars for the ten-dollar haircut you used to get for five dollars when you had hair.”

– Sam Ewing

Merriam-Webster defines inflation as “a continuing rise in the general price level.” To go a bit further, there are two main types of inflation: demand-driven (where consumer-driven demand for goods and services is greater than supply) and cost-driven (cost increases in goods and services where there is no available suitable alternative to consumers). An example of each: pandemic government stimulus spending could lead to demand-driven inflation by boosting the money supply quickly without a corresponding bump in supply. Cost-driven inflation could appear when oil production costs rise, which are then passed along to consumers.

Why is the concept of inflation so important? Because it affects just about everything, including interest rates, the return on your investment portfolio, and the prices of gas and groceries. It is important enough that the Federal Reserve uses it as one of two key considerations (along with employment in setting short-term interest rate policy). The Fed has historically targeted 2% as their desired inflation rate; however, inflation has been subdued since the financial crisis of 2008. As a result, the Fed recently signaled a willingness to allow inflation to run above target longer before adjusting interest rates – but only when following an extended lower-inflation period.

Thus far, during the recovery, the Fed has kept short-term rates near zero, and has signaled it will keep them there through 2023. But the Fed does not directly control longer-term interest rates, which are largely a function of expectations for growth and inflation. These longer-term rates have recently increased. Even though these rates are not elevated by any historical standards, the move has caused some market angst. The concern is that if economic growth expands too quickly and inflation rises significantly, the Fed will be forced into raising short-term rates sooner than expected.

Many economists believe that the Fed has historically done a poor job of timing rate hikes, and that the recovery could be prematurely stifled if the Fed acts too soon coming out of the pandemic.

The potential for higher inflation has led to some recent volatility in stock prices. However, the effect on bonds has been more pronounced. Inflation and rising rates can affect bond returns in two ways: decreased purchasing power of interest payments, and potential price depreciation as existing bonds become less appealing than newly issued ones. But some perspective is in order. A bad year in bonds typically sees low-to-mid single-digit percentage losses, whereas a bad year for stocks generally is much worse. A silver lining to increasing interest rates for bond investing is that higher interest payments on newly purchased bonds help to offset lower interest payments and price fluctuations of older bonds.

Our suite of active bond funds seeks to anticipate future inflation and interest rate moves and position their portfolios accordingly in an attempt to outperform the general bond index. With rates likely rising, it will be challenging to replicate last year’s returns of bonds in the foreseeable future. However, the rationale for including bonds in portfolios remains valid: to diversify the risk from stocks and provide ballast against stock market volatility.

POSITIONING

Our view is that economic growth will accelerate in 2021, especially in the second half of the year, as the aggressive and robust vaccination effort reaches a high enough level to promote a sense that normal activity can resume. A sizeable amount of the more than four trillion dollars appropriated through government stimulus has already filtered into the economy. Bloomberg estimates that more than a trillion additional dollars of excess savings are held in the United States. A significant portion of this money is likely to be spent as the pandemic recedes, satisfying the pent-up demand of millions of consumers for travel, entertainment, dining out, and other pandemic-restricted activities.

Although all this anticipated economic growth and consumer spending may cause a short-term increase in year-over-year inflation metrics (when compared to the 2020 pandemic depths), we do not anticipate sustained elevated inflation levels over the next year for two main reasons:

1. Unemployment remains elevated due to the pandemic, evidenced by both the official unemployment rate and the increased number of individuals who left the workforce entirely. While this slack remains in the labor market, businesses should see employee wages remain relatively consistent and experience less upward pressure on their overall costs.

2. Even if GDP growth is strong in 2021 as projected, U.S. total economic output remains below the pre-pandemic trendline. This gap would likely need to be made up before sustained inflationary pressures would begin to build.

The longer-term outlook for inflation is slightly more concerning. If elevated economic growth and massive government spending continue for an extended period, the perfect storm of inflationary triggers could arise if employment numbers and productivity spike. While this is unlikely in the very near future, we are constantly examining these data points for clues on what the future may bring.

Regardless of the outlook for economic growth, inflation, stock prices, and interest rates, we remain committed to our core investment tenets of asset allocation, global diversification, cost sensitivity, and using a carefully constructed financial plan to inform investment decisions. This is the foundation upon which your portfolio is built.

Please contact us with questions or to chat!

Jim Long, CFA, CFP®, CMFC®

Director of Investments

You can follow us on YouTube, LinkedIn, Facebook and Twitter.