Filing for Social Security benefits may be one of the most important financial decisions you make. It’s also one of the hardest. The variables to consider include longevity, continued employment possibilities, cash flow needs, retirement savings, and spousal or survivor benefits. This is why it’s such a challenge to decide when and how to file for Social Security. So, how do you optimize your benefit?

Let’s first better understand how Social Security works. Your Social Security retirement benefit is based on your earnings history and number of years worked, also known as “credits.” Your benefit is calculated by the highest 35 years of your earnings history and the result is called your primary insurance amount (PIA). PIA is the monthly dollar amount payable at your full retirement age (FRA), which currently ranges from age 66 to 67 based on your birth year.

Social Security retirement can begin as early as age 62 and as late as 70, but the monthly amount you’ll receive is reduced if you elect prior to your FRA. Additionally, your Social Security retirement grows with inflation, called cost-of-living adjustments (COLAs). The Social Security COLA is based on the dollar amount you first receive. So, the later you elect to receive Social Security, the larger your monthly check will be.

Let’s review an example to see what starting age would optimize Social Security for a fictional client, Susan.

The Facts:

- Our client Susan is single, retired, about to turn 62 years old, and has a PIA of $1,000/month at her FRA of 66.

- Susan would like to begin collecting Social Security as early as possible but isn’t sure if that is wise.

*Social Security COLAs are not included in this example.

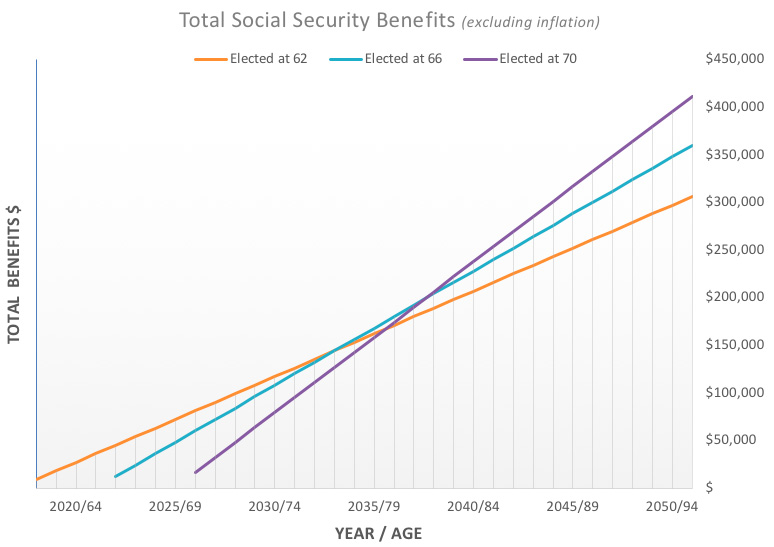

If Susan begins receiving Social Security at age 62, she will receive a reduced benefit of only 75% of her PIA, or $750 per month. The Social Security Administration reduces the monthly benefit since Susan would likely receive payments over a longer period of time. If Susan waits until her FRA, 66, she will receive the full $1,000 PIA per month. On the other hand, if Susan defers until age 70, she would collect an 8% per year (or 32% total) increase on her PIA as a reward for waiting. Her age 70 payment would be $1,320 per month. This chart below shows the total Social Security received at different starting ages (excluding inflation) over Susan’s lifetime:

As you can see, the lifetime amounts can be significantly different. However, Susan doesn’t know how long she will live. Longevity is the primary factor in optimizing her Social Security. On the chart, you’ll notice points in time where Susan’s age 62 total benefit is surpassed by the total benefits of waiting until FRA (66) or 70.

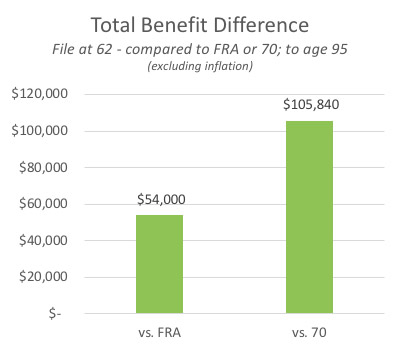

Let’s assume Susan lives to age 95. Should she claim at age 62 or later?

Obviously, age 70 is the optimal choice for Susan, assuming she lives to 95. However, in a real-life situation, longevity is unknown.

Understanding your options and knowing the facts is critical to optimizing your benefit. Go to ssa.gov for more information and to review your Social Security benefit. You may also call me for help. My goal is to guide you through the process so you have clarity and confidence in your decision.